Quick answer

If you’re paid every other Friday, your 3 paycheck months in 2026 are January and July (first payday Jan 2) or May and October (first payday Jan 9). July’s third check lands July 31, 2026. Smartest first move right now: high-interest debt — the average card that carries a balance is charging 22.15% (Fed G.19 data, Q2 2026).

Here’s a fun payroll glitch that works in your favor for once: if you’re paid biweekly, two months a year hand you a third paycheck. Twenty-six paydays don’t divide neatly into twelve months, so twice a year the calendar hiccups and an entire extra deposit shows up.

And here’s the sad part. Most people can’t tell you where that check went. It arrives, it mingles with the regular money, and three weeks later it’s just… gone. A whole paycheck, absorbed by nothing in particular. If July is your lucky month, that third check hits July 31 — which gives you about two weeks to make a plan so this one actually does something.

Key takeaways

- Paid biweekly on Fridays? Your 2026 three-paycheck months are January + July or May + October, depending on your first payday of the year.

- The third check isn’t a bonus — it’s your normal pay. But because monthly budgets can’t see it, it usually vanishes.

- Best order of operations: high-interest debt → emergency fund → sinking funds → a guilt-free slice of fun.

- Decide where the check goes before payday. Unassigned money always finds a way to leave.

Which months have 3 paychecks in 2026?

It depends on one thing only: the date of your first paycheck of the year. Biweekly pay means a check every 14 days — 26 per year — and since most months only fit two, the two “overflow” checks land in specific months you can predict to the day.

| Your first 2026 payday | 3 paycheck months | The three paydays |

|---|---|---|

| Friday, January 2 | January & July | Jul 3 · Jul 17 · Jul 31 |

| Friday, January 9 | May & October | Oct 2 · Oct 16 · Oct 30 |

Paid biweekly on a Thursday or another weekday? Same logic — grab your pay schedule, mark every payday on a calendar, and look for the two months with three marks. It takes two minutes, and honestly it’s a little thrilling, like finding money in a coat pocket six months in advance.

Quick 2027 preview while you’re at it: first payday Friday, January 1 → January and July again. First payday January 8 → April and October. Put it in your calendar now and future-you gets to look forward to it all year.

Why the third check always disappears

This is the part almost nobody talks about, and it’s the whole game: a monthly budget literally cannot see a three-paycheck month.

Think about how most budgets work. You write down your monthly income, your monthly bills, your monthly savings goal. But if your “monthly income” line says the same number every month, the extra check never appears anywhere on paper. It slides into your checking account off the books — and money that isn’t on the books gets spent. Not on anything memorable, either. It leaks out through takeout, little Amazon orders, and “eh, we’re doing fine this month” energy.

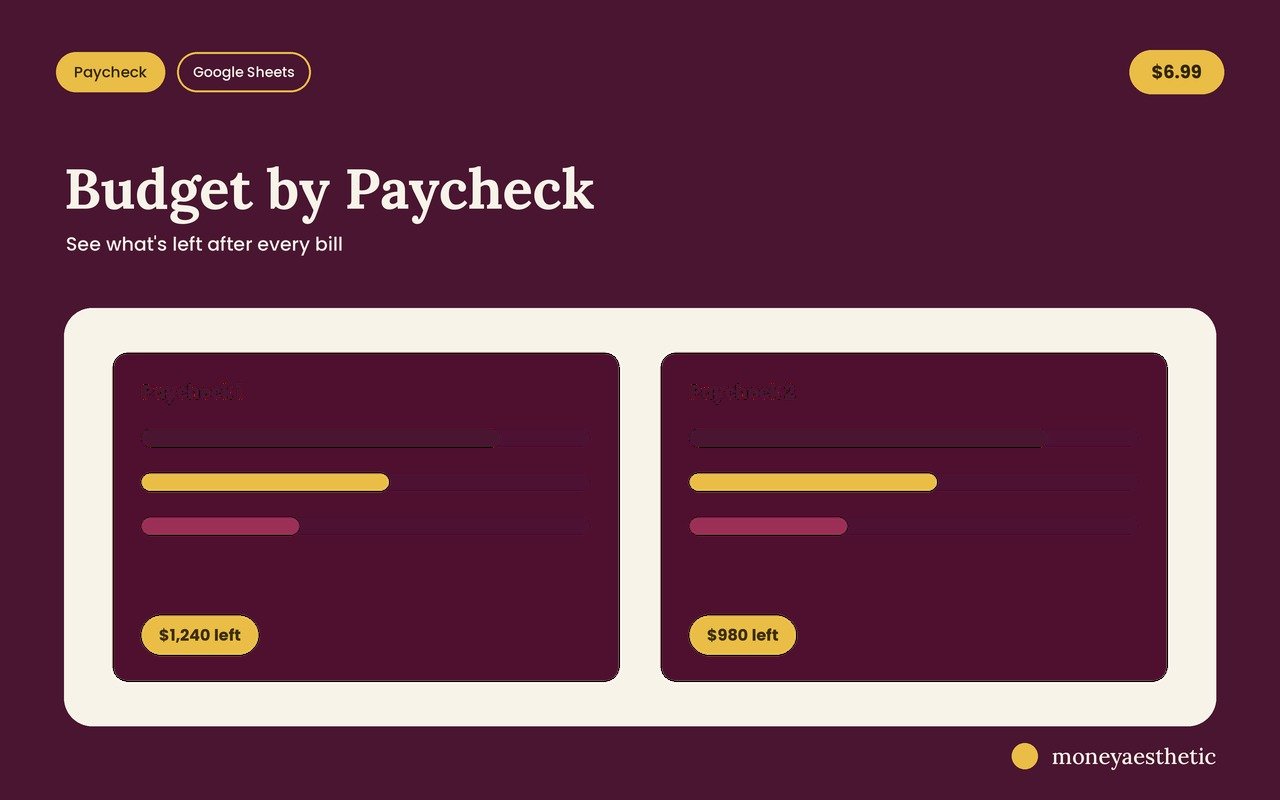

The fix is to budget by paycheck instead of by month: every time a check lands, each dollar of that specific check gets a job — these bills, this much to savings, this much to spend. Suddenly a third check isn’t invisible. It shows up as a glorious column where almost nothing is owed, and you get to decide on purpose what all that margin does. (This is exactly what our budget by paycheck spreadsheet automates — you type your paydays and bills once, and it shows you what’s safe to spend or send to goals from every single check, including the magical third one.)

If you’ve read our guide on how to stop living paycheck to paycheck, this is the same principle wearing a party hat: match your money to your actual pay schedule and the chaos stops.

What to do with the extra paycheck (in order)

The classic advice is “save it,” which is about as useful as “eat better.” Here’s an actual sequence. Work down the list until the check runs out.

- Kill high-interest debt first. Americans are carrying $1.25 trillion in credit card balances as of Q1 2026, per the New York Fed’s Household Debt and Credit report, and the average card that’s accruing interest charges 22.15%. No savings account on earth pays you 22% — so if you have a balance, throwing the third check at it is the single highest-return move available to you. Not sure which balance to hit? Here’s which debt to pay off first.

- Pad the emergency fund. No card debt? Beautiful. Park the check in a high-yield savings account. One extra paycheck can add weeks of breathing room, and breathing room is the difference between “annoying surprise” and “financial crisis.”

- Front-load a sinking fund. Holidays, car registration, back-to-school, that wedding you already said yes to — future expenses you can see coming. A third check can fund an entire sinking fund in one shot, which means December-you pays for the holidays with cash instead of a credit card hangover.

- Spend a slice on purpose. Seriously. Give yourself 10–20% of it, guilt-free. A plan with zero fun in it is a plan you’ll abandon, and this way the fun is a line item instead of a leak.

One more insider tip: peek at your pay stub. Many employers only take benefit deductions (like health insurance) out of the first two checks each month, so check #3 sometimes lands a little fatter than normal. Check with your payroll people so the surprise doesn’t go the other way.

Never lose a paycheck again

The Budget by Paycheck template shows you exactly what’s safe to spend from every check — bills covered first, goals funded, fun money included. Type your paydays and bills once; it does the math forever. Third paychecks show up in lights instead of disappearing.

Get Budget by Paycheck →Common misconceptions

“The third paycheck is extra money.” It’s not — and knowing this actually helps. You earn the same annual salary whether it arrives in 24 slices or 26; the calendar just bunched two months up. The real opportunity is that your regular monthly bills are already covered by the other two checks, so check #3 arrives with almost nothing pre-claimed. Not extra money — extra margin.

“Everyone’s three-paycheck months are the same.” Nope. Half of biweekly America gets January/July 2026, the other half gets May/October. It’s purely about your first payday of the year, which is why your coworker is smug in July and you’re smug in October.

“I’m paid twice a month, so I get one too.” Sadly, no. Semimonthly pay (the 15th and the last day) is exactly 24 checks — tidy, predictable, and extra-check-free. Your consolation prize: your checks are each slightly bigger all year long.

“You have to be responsible with 100% of it.” The all-or-nothing mindset is why most money plans die. Assign every dollar, yes — but “fun” is a legitimate assignment. A planned 15% treat beats an unplanned 100% vanishing act.

The two-week head start (do this before July 31)

Money that arrives without a plan gets absorbed; that’s just physics. So the actual work happens before payday:

- Open your budget (or grab our free monthly budget template if you don’t have one yet — it costs nothing).

- Write the third check into it as its own income line. It’s real now. It’s on the books.

- Pre-assign every dollar using the order above — debt, cushion, sinking funds, fun slice.

- On payday, move the money within 24 hours. Speed is the whole trick; margin that sits in checking gets eaten.

Ten minutes of planning, and 2026’s payroll glitch turns into the most satisfying financial win of your year — twice.

FAQ: 3 paycheck months in 2026

What are the 3 paycheck months in 2026?

For biweekly Friday schedules: January and July if your first 2026 payday was January 2, or May and October if it was January 9. July’s three paydays are July 3, 17, and 31.

How do I figure out my own three-paycheck months?

Mark every payday on a calendar and find the two months with three marks. Every biweekly schedule has exactly two of them — 26 checks just don’t fit evenly into 12 months.

Is the third paycheck extra money?

Technically no — it’s your normal pay, sliced differently by the calendar. But since your monthly bills are usually covered by the first two checks, the third arrives with almost nothing claimed. Extra margin, not extra money.

What should I do with it?

In order: high-interest debt (average interest-accruing card = 22.15% right now, per Fed G.19 data), then emergency fund, then sinking funds, then a guilt-free fun slice of 10–20% so you actually stick to the plan.

Do semimonthly employees get a three-paycheck month?

No — paid on the 15th and last day means exactly 24 checks a year. The upside: each of your checks is a bit bigger than a biweekly one all year.

Is July 2026 a three-paycheck month?

Yes, for half of biweekly America — anyone whose first 2026 payday was January 2. Those July paydays: July 3, 17, and 31. The other half gets theirs in May and October.

Why is my third paycheck sometimes bigger?

Lots of employers take benefit deductions (health insurance, etc.) from only the first two checks each month. If yours does, check #3 lands slightly fatter. Ask payroll before you count on it.

What are the 3 paycheck months in 2027?

Friday biweekly: first payday Jan 1, 2027 → January and July. First payday Jan 8, 2027 → April and October. Calendar them now; it’s a nice thing to look forward to.

This article is for general information only and isn’t financial advice. Your situation is unique — for personal guidance, talk to a qualified financial professional.